Global oil demand will decline this year for the first time since Covid-19 shut the world down in 2020. That is the headline finding from the International Energy Agency's April oil market report, released Monday, and it marks a turning point in a crisis that has already sent prices on the wildest ride in a generation.

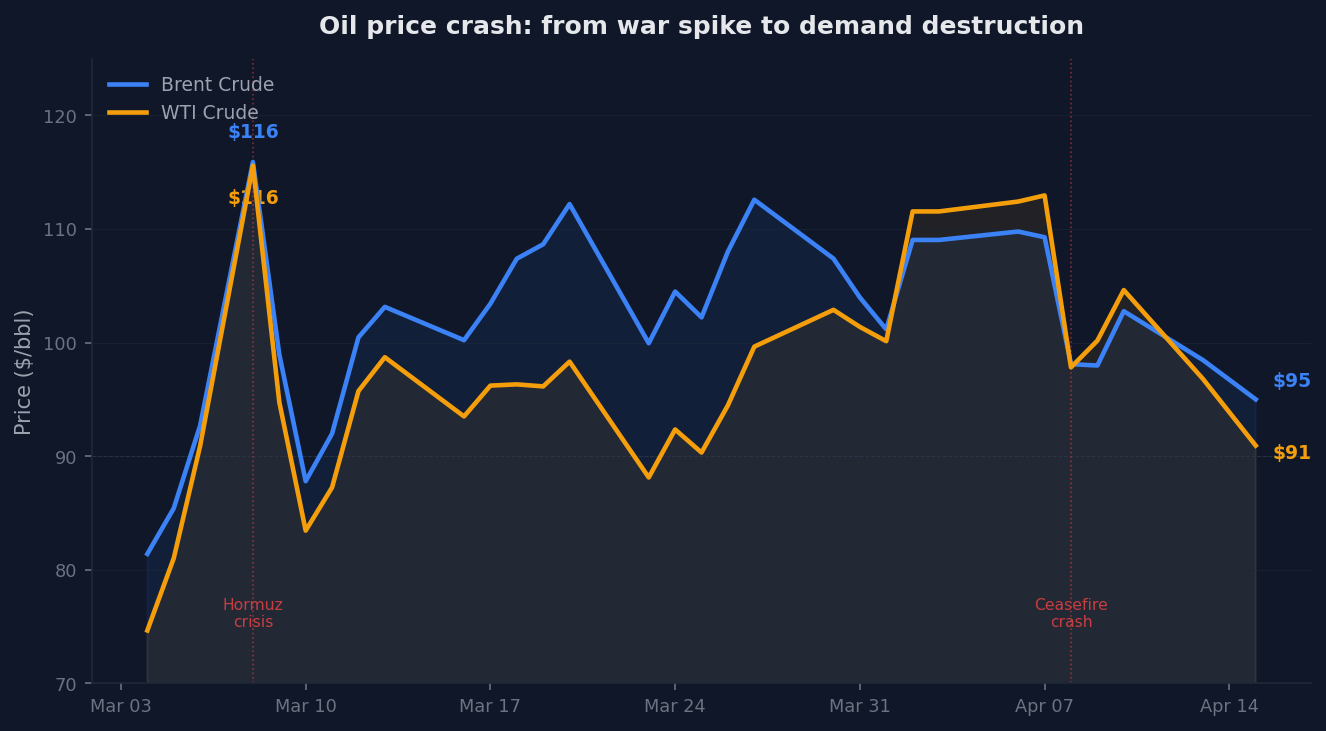

Brent crude traded at $95.00 a barrel on Tuesday. WTI sat at $90.93, down from physical-market peaks near $150 just weeks ago. The drop from those highs now exceeds 35%.

From supply shock to demand collapse

The IEA's numbers tell a blunt story. Global oil demand is now expected to contract by 80,000 barrels per day across 2026, a swing of 730,000 bpd from last month's forecast of modest growth. In April alone, year-on-year consumption is projected to fall by 2.3 million bpd.

That second-quarter plunge of 1.5 million bpd would be the steepest since the early months of the pandemic.

"Demand destruction will spread as scarcity and higher prices persist," IEA chief Fatih Birol warned. The agency urged governments and businesses to "brace for significant disruptions in the months to come" if the Strait of Hormuz stays choked.

Three sectors bearing the worst pain

Aviation has been hit first and hardest. By early April, roughly 7,050 flights were scrubbed on a single Monday, about 7% of all scheduled routes worldwide. Cancellations are concentrated across the Middle East, South and Southeast Asia, and parts of Europe where jet fuel supplies have thinned out.

Petrochemicals follow close behind. Naphtha and LPG crackers across Asia are running well below capacity after Gulf feedstock shipments stopped arriving. Some plants that operated at full tilt a year ago have gone idle.

Refining rounds out the damage. Refiners in the Gulf and across Asia that depend on regional crude have pulled back hard, stripping about 6 million bpd from global throughput and dropping it to 77.2 million bpd. The IEA now sees full-year runs averaging 82.9 million bpd, roughly 1 million bpd less than last year.

Supply losses unlike anything on record

The demand destruction did not happen in a vacuum. Global oil output plunged 10.1 million bpd in March to 97 million bpd, the largest supply disruption the IEA has ever recorded. OPEC+ production alone fell 9.4 million bpd in a single month as Iraqi output dropped 67%, Saudi volumes slid from 10.4 to 7.25 million bpd, and Kuwaiti barrels nearly halved.

Strait of Hormuz loadings averaged just 3.8 million bpd in early April, down from more than 20 million bpd before the conflict. Alternative pipeline and port routes can handle roughly 7.2 million bpd, far short of replacing the missing barrels.

Global observed inventories fell 85 million barrels in March. Stocks outside the Gulf were drawn down by 205 million barrels, though some of that crude ended up trapped in floating storage near the blockade zone.

Why futures fell anyway

Physical crude, the actual barrels changing hands, still commands prices around $130 a barrel, according to North Sea Dated assessments. Singapore middle-distillate cracks hit all-time highs above $290 a barrel.

But futures markets look forward, and what they see is a ceasefire that might hold, renewed US-Iran diplomacy, and demand that is being permanently destroyed by triple-digit prices. Hedge funds that piled into oil longs during five weeks of war are unwinding fast. The result: a $50-plus gap between physical barrels and the paper market.

What comes next

The ceasefire between Washington and Tehran expires on April 22. Pakistan has offered to host a second round of face-to-face talks after last week's 21-hour session in Islamabad ended without a deal. President Trump said Monday that Iranian officials had reached out wanting to negotiate, though Tehran's public rhetoric has not softened.

If diplomacy fails and the strait stays shut, the IEA's already grim demand forecast could worsen. Reports that some governments have begun stockpiling fuel and blocking exports add another layer of risk, threatening to turn a regional shortage into a worldwide scramble.

If a deal holds, the market faces a different problem: hundreds of millions of barrels of strategic reserve oil already released, damaged Saudi pipeline infrastructure that will take months to repair, and a global economy still nursing the wounds of $150 crude.

Either way, the IEA's verdict is clear: this crisis has crossed from supply shock into outright demand destruction, and getting consumption back on track will not be quick.